Life memberships

About 15 years ago, I all but spat out my coffee when my wife mentioned in passing that she’d bought us a joint life membership for the UK National Trust at a cost of £1,380 (we subsequently also joined English Heritage on pretty similar terms).

Personally, I felt it was a lot of money considering we spent most of our time in Australia and Asia; my better half said it was a smarter idea to think of it as a donation.

This was brought to mind on a recent European summer trip across England and Wales, when, in the glorious Warwickshire countryside, we took in a couple more of the Trust’s 500 or so properties.

I noted during one such stately home visit that a dual life membership now costs around 80% more at £2,520.

Incidentally, Australia also offers National Trust memberships, the price of which has increased 4-fold since 1993, according to my research (read: Googling).

Fortunately over the years we’ve made very good use of the lifetime passes, thus allaying my fears of outlandish financial wastage, while allowing Heather to tell me that – not for the first time – that she was, and I quote, “right all along”.

Anyway, hopefully over the next 15 years and beyond we’ll get plenty more use from them…

A bird in the hand

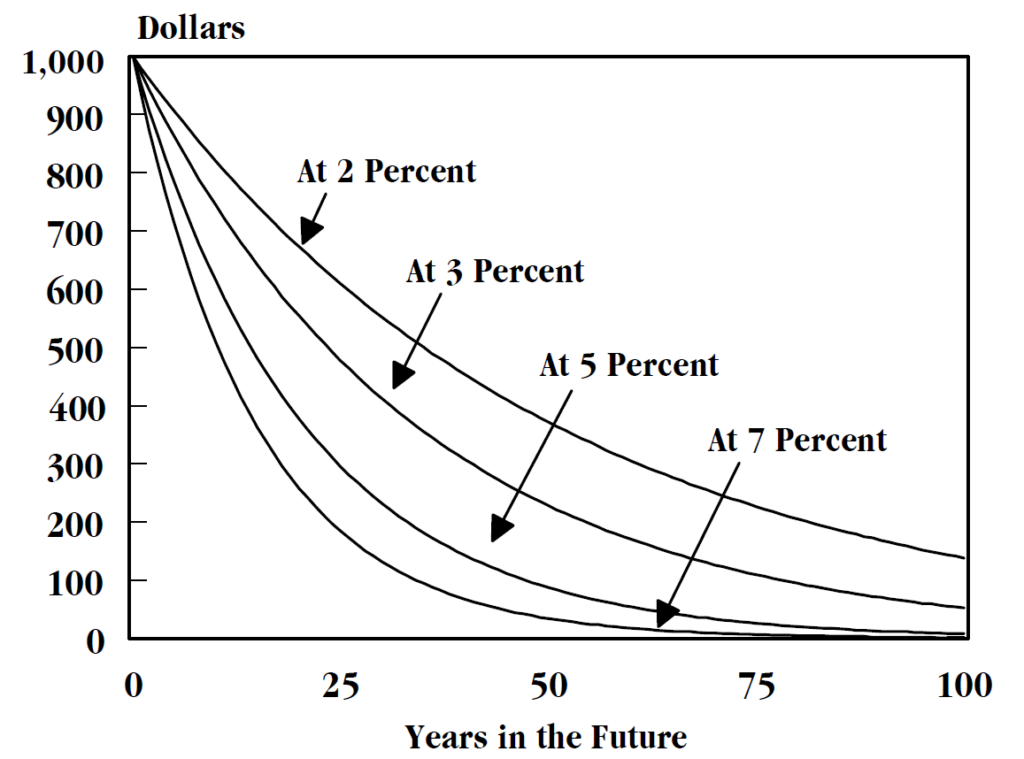

The time value of money is a fascinating concept when you dig into it.

As kids we were often taught to save our pocket money for something or other in the future, which is a useful exercise because it helps us to learn how to practice delayed gratification.

On the other hand, the reality is that $100 saved in a money box is going to be effectively worth less a year or two from now – and potentially significantly less – as the cost of goods and services rise.

Or, to put that in other words, a dollar today is better than a dollar tomorrow.

A dollar today is even more valuable to us if it can be invested wisely to become worth significantly more in the future.

Source: Investopedia

When valuing a business, an analyst will attribute a significantly reduced value for profits expected to be earned a decade from now, to discount the future dollars into a present value.

This discounting partly reflects uncertainty, and the risk that the earnings never eventuate.

Discount rates used by investors may also reflect an opportunity cost, representing what they might have achieved with the money elsewhere instead.

Everyone a millionaire!

Here’s an interesting thought.

If we earn, say, $200,000 in a year, pay about 50% of it in tax, and take home $100,000, then we need to think quite carefully about the opportunity cost of what those dollars could be earning for us in investments before spending them, which can happen all too quickly.

One of the traps to watch out for when planning your financial future is the tropes of wisdom that go something like this:

“If you invest just $400 per month and get a 7% return every year then in 40 years’ time you’ll be a millionaire thanks to the awesome power of compound interest!”.

This is sound advice…up to a point (assuming investment markets don’t unexpectedly underperform or suddenly plunge in 39 years’ time, that is!).

However, do consider that if inflation averages 4% per annum, then your $1 million will feel more like about $200,000 in today’s dollars, due to inflation or the rising cost of living…about 80% less in real terms, and nowhere near enough to retire on.

What to take away from this?

There are a few options to consider.

You’ll probably need to earn more over time as your career progresses or business grows, invest more as your income increases, and invest twice as much if you’re in a couple!

Debt and inflation

My wife Heather rarely tires of telling me how her first mortgage was around £60,000 ($120,000), a crippling some of money at the time which required lodgers to help her make the repayments, and yet a figure that 3 decades on you could feasibly bung on a couple of credit cards.

I’ve always felt that one of the neatest things about property as an asset class is that you don’t need to put nearly as many of your own dollars into the investment to build a very large portfolio.

It’s true that this requires some smart decisions are careful management of debt and risk.

But over time you’ll find that even very large mortgage balances are steadily inflated away (while modest capital growth of 4-5% per annum can create spectacular results over long periods of time).

Real estate is on only asset class where everyday individuals can borrow large sums of money, for very long periods of time, and at comparatively low interest rates…and without a high risk of the loan being called in by the lender.

Once you understand the time value of money, you may well consider many financial decisions differently, from student loans to car purchases, wedding costs, home renovations, holidays, school fees, pension contributions, and more.